4. Benefits of TBhC initiatives

4.1 Overview

As discussed in Section 2.3, existing users of individual transport modes generally do not receive a benefit in TBhC project appraisals. If some components of a TBhC package do result directly in a change in generalised cost for existing users of the affected mode, these are considered 'hard' initiatives and should be analysed with the relevant PT and active transport guidelines. With 'soft' TBhC initiatives, only the travel behaviour changers will receive a benefit (or they would not make a change). Since this cannot be estimated by the traditional 'rule of half' method from existing user benefits, an alternative valuation approach is required, as described below[1].

The alternative user benefit estimation approach is based on users’ perceived costs so overall project benefits also need to include resource cost corrections for unperceived resource costs as well as externality benefits.

4.2 Benefits to mode changers

Section 2.3 explained that the perceived benefits to mode changers are a valid benefit to estimate and include in the economic appraisal of TBhC projects. This approach is consistent with theory incorporated in transportation planning modelling and in the assessment of benefits to induced traffic. This section discusses the derivation of appropriate values for use in TBhC project appraisals.

In a 2004 ATRF paper, Winn (2004) described a method and derived estimates of the benefits perceived by mode changers from the mode split relationships incorporated in strategic transport planning models. These relationships reflect the change in mode shares between two modes that will result from changes in the relative perceived generalised costs of the two modes.

The mode split between two modes is a function of the difference in perceived generalised cost between the two modes. The relationship can be used in reverse to determine the change in perceived generalised cost difference that is required to achieve an observed change in mode share. Because the mode share relationships in the transport models are calibrated to actual observed travel choices, this generalised cost difference can be equated to the perceived benefit associated with a given change in mode share.

Winn described the estimation process as follows:

"For the valuation of the user benefits associated with changes in the mode of travel a logit based mode split model is used. This model form is commonly used in four stage strategic transport models to allocate trips between motorised and non-motorised modes and between public transport and motor car within the motorised category. The market share of one mode compared to another is a function of the difference in generalised cost, with a slope parameter governing the rate of change and a shift parameter included to take account of the attributes not included in the generalised cost formulation.

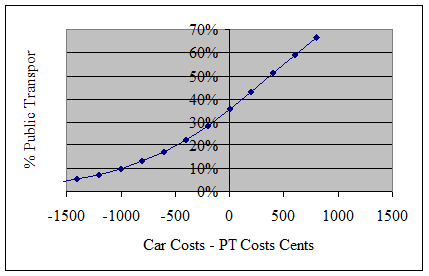

Figure 3 illustrates the public transport share of motorised transport using typical parameters found in the Melbourne Integrated Transport Model (2000). Notice that where there is no difference in generalised cost public transport accounts for 35% (not 50%) of trips. This reflects the inherently superior comfort and convenience attributes of car-based travel (that are not accounted for in the generalised costs).

As a further illustration; if the current public transport mode share of motorised travel was 10% (which occurs if public transport costs are $10 more than car costs), then a reduction in public transport costs relative to car of about $5 (500 cents) would be required to raise the public transport mode share to 20%.

Figure 3: Public transport mode share of motorised travel

This information can be used in the following way to infer a value for the user benefits of those who switch from car to public transport for the same type of journey:

- in the example TBhC application considered, a 15% increase in public transport trips and a consequent increase in the public transport share of motorised trips from 13% to 17% was assumed (i.e. a four percentage point increase in public transport mode share); this is consistent with experience in Australia and internationally;

- applying the relationship shown in [Figure 4] suggests a change in the generalised costs of public transport compared to car of around $2 (200 cents) would be required to effect this shift, and

- the rule of half should be applied to set the average benefit per user at half the full benefit (a downward sloping demand curve implies that some (marginal) car users would require only a small change in cost to switch while some would require the full $2 shift to move).

A similar approach may be followed to value the benefits for those switching from car travel to walking and cycling. This analysis assumes a 10% increase in walk trips and a 75% increase in cycling (from a low base), raising the walk/cycle share of all trips from 25% to 29% (a four percentage point increase in active transport mode share). The Melbourne Integrated Transport Model parameters suggest a change in relative generalised cost of about $1.50 is required to achieve this change indicating that the average benefit for those switching is $0.75.â

For these Guidelines, the analysis described above has been generalised to derive mode changer perceived net benefit values for TBhC initiatives that result in different diversion rates than the 4 percentage point diversion assumed in Winn’s example.

A similar approach was used to derive mode changer benefits during development of the New Zealand TBhC appraisal procedures. This gave similar benefit values to those obtained by Winn. The Winn values were also reviewed and reaffirmed in a TravelSmart economic analysis for the Victorian Department of Infrastructure in 2006 (Maunsell, 2006).

Table 7 shows the proposed perceived net benefit values to be used for mode changers following further review of the above analysis. These values have been updated to 2014 from the values derived earlier and rounded slightly, reflecting the degree of approximation in the methodology for their estimation.

| Mode change | Size of mode change (percentage points) |

Benefit ($/trip) |

| Car driver/passenger to public transport | ||

| 1 | $0.35 | |

| 2 | $0.70 | |

| 4 | $1.40 | |

| Car driver/passenger to cycle/walk | ||

| 1 | $0.25 | |

| 2 | $0.50 | |

| 4 | $1.00 |

It is proposed to use the same benefit values for peak and off-peak periods because the model relationships produced little difference or were not reliably different. Values for other percentage point changes in mode share may be interpolated or extrapolated from Table 7.

Consideration was given to whether different benefit values may apply in cities with less extensive public transport choices but again evidence was not available to confirm or refute this. There appears little reason for the values for people changing from car driver/passenger to cycle/walk to vary by location as the perceived benefits are likely to be similar wherever they occur.

It is worth restating that the mode changer perceived net benefit values in Table 7 are the net total of all the savings and costs that the average mode- hanger perceives they are incurring when changing to the new mode. As these values are derived from a multi-modal transport network model, they incorporate the net saving across all the usual perceived cost components that are included in the private generalised costs of the 'from' and 'to' modes in such models. For example, for highway trips the components include travel time, fuel, tolls and perceived parking charges. The values also include any other intangible perceived benefits and costs that are not specifically itemised in the model but that are incorporated in the logit model and calibration factors that are used to ensure that the transport model reflects observed mode choice decisions and mode shares.

Previous studies have noted that the method and detail of obtaining benefit values from mode choice relationships is still evolving and suggested the following issues for further consideration and investigation:

- It is likely that the mode choice relationship will change as a result of the TBhC project itself - that is, the position and slope of curve may change from that represented in the strategic transport model and therefore indicate different benefits.

- We might not be measuring the slope at a point on the curve that is representative of mode changers. Changers might tend to come mostly from a particular (flatter or steeper) part of the curve.

- More information is needed on how the mode choice models are constructed. The statistical validity of the curve will depend on how much detailed survey data on actual travel characteristics and choices has been used to calibrate the model.

4.3 Resource cost corrections

This section discusses the benefit and disbenefit components that are internal to (that is, directly affect) mode changers but that are not fully perceived and included in the mode changer net benefit values in the previous section.

One of the main ways that TBhC projects seek to change travel behaviour is by informing and educating travellers about the full costs of travelling by different modes, particularly by private car. It follows that the 'misperception' of resource costs by travel behaviour changers is likely to be less in the Project Case than without the TBhC project and, therefore, that different resource cost correction values might be required for TBhC projects than for public transport and active transport projects that do not include such information and education aspects.

The following paragraphs discuss each of the normal benefit categories, whether they require resource cost corrections and whether TBhC project-specific resource cost corrections need to be derived. Suggested default parameter unit values for resource cost corrections and externalities are summarised at the end of this section.

4.3.1 Travel time savings

Travel time savings (or increases) do not need to be assessed directly when using the recommended perceived cost approach because travel time changes and related impacts are considered to be fully internalised in the mode changer net benefit values estimated in the previous section. This includes effects such as differences in travel time by different modes, differences in the value of that time, other time costs such as waiting and transfers, and trip time reliability. All of these tend to be readily taken into account by users based on their experiences and directly influence their mode choice and other travel behaviour decisions.

4.3.2 Private vehicle operating costs

A proportion of vehicle operating costs are perceived by motorists and hence taken into account in their mode choice decision. However, it is normally considered (and reflected in multi-modal transport models) that motorists only perceive the fuel component of vehicle operating costs. Therefore, in public transport economic appraisals, a resource cost correction is required for the difference between this and total VOC resource costs avoided as a result of motorists' mode change. Furthermore, fuel costs are perceived in market prices that include fuel excise duty and indirect tax (GST), which are not resource costs.

Accordingly, the resource cost correction for reductions in private vehicle operating costs normally includes two components:

- A positive correction for the unperceived non-fuel resource costs

- An offsetting negative correction for the duty and tax proportions of fuel costs that are part of perceived cost, but are not resource costs.

One of the objectives of TBhC projects is to provide information that corrects people’s misperceptions of the costs of private car use. For TBhC project appraisals, it is assumed that TBhC projects will provide sufficient information to make users aware of a greater proportion of the previously unperceived vehicle operating costs and hence their perceived costs will be equal to resource costs[2]. A VOC resource cost correction of zero should therefore be adopted for TBhC projects.

4.3.3 Car ownership costs

Car drivers who transfer to public transport and/or cycling and walking may be able to avoid the need to own a car due to the change in mode. If this is the case, and given the general conclusion that motorists do not perceive vehicle depreciation or the opportunity cost of capital when making individual travel decisions, a resource correction is normally needed to take account of the additional, unperceived resource saving. However, for similar reasons to private vehicle operating costs, the resource cost correction for reduced car ownership should be set to zero for TBhC projects.

4.3.4 Car parking

Reduced car use results in a reduction in the demand for parking facilities. The resource costs of car parking include the opportunity cost of using land for parking, the capital cost of parking facilities and the provision of adequate security.

Motorists are charged a fee for the use of parking. This charge differs depending on the destination of a journey and the time of day that the journey is made. Parking charges are higher for trips to the CBD and during peak times, and lower for off-peak and non-CBD trips. For many commuters, car parking is subsidised or provided free by employers. Also, many businesses, shopping centres and other destinations provide free parking. Overall, the parking fees paid by car users are less than the resource cost of providing parking. Motorists who change to public transport or active modes are likely to consider only the parking fee that they actually save in their perceived net benefit. People are assumed not to be aware of, or take account of, any difference between the fee they pay and the actual resource cost of providing the parking facilities, so a resource cost correction is required for this difference.

In the absence of specific research it is normally estimated that, on average, only about 50 per cent of car parking resource costs are perceived. Hence, a resource cost correction equal to the remaining unperceived 50 per cent is applied.

Some cities impose CBD parking levies that partially or wholly offset this difference. These should be taken into account when determining resource cost corrections for car parking.

Some of the strategies included as part of TBhC projects are measures to make car users more aware of the full costs of car parking, so it is assumed that TBhC projects will reduce the misperception of car parking resource costs and hence the required resource cost correction will be less than for public transport projects. Nevertheless, many commuters will continue to benefit from car parking that is subsidised or provided free by employers and hence will not perceive any change.

For TBhC project appraisals it is assumed that, on average, TBhC initiatives will reduce the resource cost misperception by a half, resulting in TBhC participants perceiving 75 per cent of resource costs after implementation of the TBhC initiative. Therefore, for each car driver trip diverted to public transport or active transport, a resource cost correction of 25 per cent of the car parking resource cost (per trip) should be included in the benefits.

The car parking resource cost per trip is obtained by dividing the daily parking resource cost by two (that is, between the inbound and return trips). The car parking resource cost correction is not applied for avoided car passenger trips, only avoided car driver trips.

4.3.5 Road tolls

A resource cost correction is required for road tolls. Tolls are charged to recover the capital and operating costs of toll roads and therefore could be considered to reflect a resource cost. However, sometimes tolls are just charged to recover the cost of purchasing a concession from the government to charge tolls on an existing road. In either case, by the time trips are made on a road the capital costs are 'sunk' and use of the road causes minimal on-going resource costs. Trucks may cause pavement wear and the road operator needs to provide traffic management and incident response functions, but these costs are small compared to the financing and amortisation of the capital costs.

It might also be argued that cars impose congestion costs on other road users in peak periods and that the tolls reflect this resource cost. However, congestion costs and reductions in congestion are explicitly estimated in an economic analysis. It would be double counting to include tolls paid by new highway users (or saved by lost users) as a resource cost in a project evaluation in addition to the congestion costs (or savings) resulting from changes in traffic volume. Each of the foregoing explanations result in the conclusion that tolls are a transfer and the resource cost of tolls is zero.

Savings in toll payments form part of the perceived benefits of toll road users who transfer to public transport and hence are included in the mode changer perceived net benefit values in Section 4.2. If a TBhC initiative will divert trips from a toll road, a resource cost correction is required because this perceived saving is not actually a resource cost saving. The resource cost correction for a trip diverted away from a toll road is a negative amount equal to the full toll saving - that is, it reduces total benefits.

From a practical viewpoint, it will usually be difficult to identify whether avoided car trips due to TBhC projects would have used a toll road, so this resource cost correction is not included in the benefit unit values in Table 8. If a TBhC initiative will significantly reduce trips on a particular toll road, the reduction in toll payments should be quantified and included as a resource cost correction.

4.3.6 Cycle operating costs

Resource cost values for cycle operating costs are provided in the mode specific active transport guidelines and/or parameter value guidance.

People changing mode from car to cycle are likely to be aware of the probable incremental cycle costs. It could be argued that, as with cars, people do not fully take into account infrequent costs such as tyres and maintenance. However ,TBhC projects typically correct these misperceptions and the same is likely to apply for cycle costs. TBhC project appraisals should assume that cycle costs are correctly perceived and taken into account in the mode changer net benefit value and therefore adopt a resource cost correction of zero for cycle costs.

4.3.7 Walking costs

In theory, these would be treated the same as cycle costs. In practice, they are ignored because they are likely to be negligible.

4.3.8 Public transport fares

A resource cost correction is also required for public transport fares. This is because fares are, in the first instance, a benefit gained by public transport users before they become a financial transfer (from mode changer to public transport operator). They are not an actual resource cost. If the public transport operator does incur additional operating costs, these are accounted for directly in the cost side of the economic analysis. The person changing to public transport perceives fares as a cost but they are not a resource cost, so it is necessary to make a resource cost correction (as a benefit) equal to the (tax inclusive) amount of fare. Tax inclusive fare is used because this is the cost that the mode changer perceives.

Analysts should use average fares for the city where the TBhC project is to be implemented. The average fare per passenger is included as a resource cost correction benefit for each trip diverted to public transport as a result of the TBhC project. An average child concession fare should be used for appraisal of school travel plans.

A fare resource cost correction is required for all trips that divert to public transport, including former car passenger trips as well as car driver trips.

4.4 Externality benefits

In addition to the internal perceived and unperceived benefits and disbenefits to travel behaviour changers, TBhC initiatives also result in externality effects on other transport system users and on society. These are discussed in the following paragraphs.

4.4.1 Decongestion

Decongestion refers to the reduced congestion costs (time and vehicle operating cost) experienced by remaining road users as a result of some car drivers changing to public transport or active transport modes - it does not include the saving to the mode changers themselves as this is part of their internalised benefit. Travel time savings provide most of the decongestion benefits, with vehicle operating cost savings typically contributing only about 5 – 10 per cent of the total decongestion benefits.

For most TBhC projects, it will be appropriate to make a simple estimate by multiplying the reduction in vehicle kilometres travelled with a unit value for congestion relief benefits in terms of cents per vehicle kilometre of reduced car travel under relevant traffic conditions. Unit values per vehicle kilometre of avoided car travel under various conditions are provided in the parameter unit values guidance/appendix.

4.4.2 Induced traffic effect

The reduction in congestion resulting from TBhC projects is likely to make car travel more appealing for other potential road users, leading to increases in car use by other individuals and thereby partially reducing the first round decongestion benefit. The induced traffic effect should be valued as a disbenefit equivalent to 50 per cent of the decongestion benefit. In other words, half of the potential ‘first round’ decongestion benefits are offset by induced traffic disbenefits. This estimate is based on research by Booz Allen, which noted that induced traffic disbenefits as high as 70 per cent of decongestion benefits were estimated for heavily congested parts of London and which recommended a disbenefit of 50 per cent for peak periods in Auckland.

4.4.3 Road system benefits

Road system benefits include the benefit of reduced road maintenance and deferral of road capacity increases. It would be valid to include road maintenance savings but these are negligible for the numbers of car trips and/or car vehicle kilometres that are likely to be removed by TBhC projects. Benefits from deferral of road capacity increases are not included because they are also expected to be negligible. Furthermore, it would not be correct to include both the value of deferring improvements and the full decongestion benefit discussed above. If the capacity improvements were undertaken rather than deferred, the congestion levels would be less and the decongestion benefit theoretically somewhat lower.

4.4.4 Accident cost savings – car

A shift of some car drivers to public transport or cycling and walking can result in a decline in the number of accidents due to fewer car-kilometres of travel. This may be offset by the change in the number and severity of accidents due to changes in road traffic conditions such as higher speeds[3].

Accident costs can be considered in three parts: internal costs (those affecting the travel behaviour changer) that are perceived and hence included in the mode changer net benefit value; internal costs that are not perceived and hence require resource cost correction; and external costs borne by others.

There is little information available on the extent to which people perceive accident risks and costs and take this into account in their travel choices. If it is considered that people take full account of the accident risk and costs to themselves, then this is already included in the mode changer net benefit value and only the externality costs need to be added. However, if people underperceive their accident costs, a resource cost correction is required. Intuitively, it is likely that people do not perceive much accident cost and therefore most,if not all, of their internal accident cost will require a resource cost correction. If this is the case, the resource cost correction plus the externality costs will equal the total resource cost of accidents.

For TBhC projects it will be appropriate to make a simple estimate by multiplying the reduction in vehicle kilometres travelled with a unit value for accident saving benefits per vehicle-kilometre of avoided car travel in relevant road traffic conditions.

4.4.5 Accident costs – cycle/walk

The same considerations apply in relation to cycle and walking accident costs as for car accident costs. Two additional considerations with cycle and walk accident costs are that people who change from car to walking and, in particular, cycling probably have some perception of the associated accident risk, so possibly some of this (disbenefit) is included in the mode changer net benefit values, and that an increase in the number of pedestrians and cyclists might actually lead to a fall in the average per kilometre accident cost per pedestrian or cyclist (referred to as the 'safety in numbers effect').

If internal (personal) accident costs are perceived and already included in the mode changer net benefit values, the required resource cost correction is zero and only the external proportion of the accident costs needs to be counted as a disbenefit. However, when cyclists and pedestrians are involved in accidents, external costs are likely to be much smaller than in motor vehicle accidents. For TBhC projects, even these costs will be offset to some extent by the 'safety in numbers effect' - so, overall, any changes in cycling and walking accident externality costs are likely to be negligible and can be assumed to be zero in TBhC assessments.

4.4.6 Accident costs – public transport

Accidents still occur with public transport, as indicated by claims made against public transport agencies by passengers and damage caused to public transport and other vehicles. In most cases, TBhC projects will not change the distance actually travelled by public transport vehicles and hence public transport vehicle accident costs attributable to the project can be assumed to be zero[4]. For TBhC packages that include increases in public transport services, and public transport project appraisals in general, accident disbenefits should be estimated using the increase in public transport vehicle kilometres and relevant resource cost unit values in the parameter unit values guidance/appendix.

4.4.7 Environmental externality reductions

Environmental externalities include local air pollution, noise and water pollution, and greenhouse gas emissions. Less car use reduces environmental costs, according to the reduction in vehicle-kilometres of travel and changes in traffic congestion. Resource cost unit values for the environmental benefits from reduced car use are presented in the parameter unit values guidance/appendix. The resource value of various environmental impacts is expressed in relation to the quantity of vehicle use (that is, car-kilometres of travel). The quantity of saved car-kilometres needs to be estimated to determine the monetary value of the benefit. As the resource value of environmental costs is not generally perceived by motorists, the benefit will be equal to the total reduction in car-kilometres of travel multiplied by the appropriate (marginal) unit resource value of environmental benefits.

Public transport vehicles also cause externalities such as noise and air pollution that impose costs on the community. As discussed above under public transport accident costs, in most cases TBhC projects will not change the distance actually travelled by public transport vehicles and hence environmental externality costs attributable to the TBhC project can be assumed to be zero.

4.4.8 Health (fitness) benefits of cycling/walking

Parameter unit values for health benefits of cycling and walking are provided in Part M2 Active Travel. For TBhC project appraisals, the health benefits of cycling and walking are considered in three components in the same way as accident savings or costs. However, unlike accident savings it seems implausible that at least some of these benefits are not perceived by mode changers and hence not included in the mode changer net benefit values. One of the main selling points of TBhC projects, that results in people taking up cycling or walking, is the promotion of the health benefits.

As an approximation, it is assumed that half of the total health benefit is perceived by the mode changer and hence already included in the mode changer net benefit values.

Consequently, only the remaining half of the benefits is explicitly included in the appraisal as a combined value covering internal unperceived benefits (requiring a resource cost correction) and/or externality benefits to society (such as avoided hospital and other health care costs). This benefit is estimated by multiplying the increase in cycling and walking distance of people who divert to active transport modes due to the TBhC initiative by 0.5 times the respective unit values for health benefits of cycling and walking from the parameter unit values guidance/appendix.

4.4.9 Other - not quantified

A number of other potential benefits are identified in some appraisals of TBhC projects but have not been quantified to date. These include:

- Reduced community severance

- More sustainable land use/urban form

- Community cohesion

- Improved security/safety to the community

- Less dependence on fossil fuels

- Viability of local shops and businesses

- Synergy with other marketing initiatives

These impacts are generally harder to quantify and include in appraisals, but some of them may be as worthwhile as some of the other quantifiable impacts. Some of these benefit types could also apply to other types of transport initiatives and some of them possibly can be achieved more effectively by more targeted non-transport policies.

4.5 Summary of resource cost corrections and externality benefits

Suggested default values for the resource cost correction and externality benefit unit values discussed in the above sections are shown in the table below.

| Peak | Off-peak | |||

|---|---|---|---|---|

| Large city1 | Other city2 | Large city | Other city | |

| Car driver per km | ||||

| VOC resource cost correction | 0.0 | 0.0 | 0.0 | 0.0 |

| Congesting externality x 0.53 | 42.5 | 11.5 | 11.5 | 0.0 |

| Accident cost externalities | 8.7 | 8.7 | 8.7 | 8.7 |

| Environmental externalities | 6.2 | 6.2 | 6.2 | 6.2 |

| Total per km | 57.4 | 26.4 | 26.4 | 14.9 |

| per trip | ||||

| Parking resource cost correction | ||||

| - trips to/from CBD | 200.0 | 100.0 | 50.0 | 25.0 |

| - trips to/from other destinations | 50.0 | 25.0 | 0.0 | 0.0 |

| Car passenger4 per km | ||||

| VOC resource cost correction | 0.0 | 0.0 | 0.0 | 0.0 |

| Congesting externality x 0.53 | 21.3 | 5.8 | 5.8 | 0.0 |

| Accident cost externalities | 4.4 | 4.4 | 4.4 | 4.4 |

| Environmental externalities | 3.1 | 3.1 | 3.1 | 3.1 |

| Total per km | 28.7 | 13.2 | 13.2 | 7.5 |

| per trip | ||||

| Parking resource cost correction | 0.0 | 0.0 | 0.0 | 0.0 |

| Public transport passenger per km | ||||

| Accident cost externalities | 0.0 | 0.0 | 0.0 | 0.0 |

| Environmental externalities | 0.0 | 0.0 | 0.0 | 0.0 |

| Total per km | 0.0 | 0.0 | 0.0 | 0.0 |

| per trip | ||||

| Fare resource cost correction | -300.0 | -225.0 | -300.0 | -225.0 |

| Cyclingper km | ||||

| Accident externality | 0.0 | 0.0 | 0.0 | 0.0 |

| Health effects | -73.0 | -73.0 | -73.0 | -73.0 |

| Total per km | -73.0 | -73.0 | -73.0 | -73.0 |

| Walking per km | ||||

| Accident externality | 0.0 | 0.0 | 0.0 | 0.0 |

| Health effects | -145.0 | -145.0 | -145.0 | -145.0 |

| Total per km | -145.0 | -145.0 | -145.0 | -145.0 |

These values are costs (resource cost corrections and externalities) per kilometre or per trip.They become benefits if a trip is avoided, or costs if a trip is added. A negative value indicates that the effect is a benefit of a new trip on that mode; for example, health effects are benefits of cycling and walking trips.

Notes:

1 Large city = population > 1 million

2 Other city = population < 1 million

3 Net congestion externality is 0.5 x congestion externality to account for induced traffic effect, which acts in opposite direction

4 Car passenger per km values are 50% of car driver values (rather than zero) to account for a proportion of trips being made specifically for the passenger

[1] To the extent that a TBhC initiative reduces car trips, remaining highway users may also receive a decongestion benefit. This benefit is estimated and included in the CBA procedure described in these TBhC guidelines. However, while this could be interpreted as an existing user benefit, it is not one that can be used with the rule of half to estimate the perceived net benefit of mode-changers.

[2] This assumption does not mean that people perceive all non-fuel costs as a result of the TBhC project. Rather they perceive enough of the non-fuel costs so that their total perceived cost, which includes fuel taxes, equals the total resource cost (which does not include the taxes). This is not a demanding assumption.

[3] In typical urban conditions, at the margin any reduction in total accident numbers due to reduced traffic volumes is likely to be offset by increased accident costs due to higher speeds. However, the effect of speeds on urban accident costs appears not to be well researched. If the two effects are assumed to be equal/opposite, there would be no net effect on car accident costs. However, if such an assumption was adopted it should apply to all urban transport economic appraisals. Hence, this issue is noted for future consideration but the conventional assumption of accident cost savings due to avoided VKT is adopted in these Guidelines.

[4] Some public transport accidents (such as slips and trips at stations and when boarding and alighting) are likely to change in proportion to the numbers of trips; however, these have been assumed to be relatively minor. This could be an area for refinement.